There are many terms used in financial independence, but none of them need to be confusing. Fat FIRE (Financial Independence, Retire Early) is one of those terms you might have heard and wondered what exactly it is. You will find that most of these subsets of FIRE all have the same ultimate goal in mind; more control over your time. Fat FIRE gives you the ultimate form of control, but it can take a long time to achieve fat FIRE and it may be out of range for a lot of us.

Fat FIRE is simply retiring early with an above-average amount of assets and withdrawing a large sum such as 100k+ per year.

Fat FIRE follows pretty much all the same rules that traditional FIRE follows, except that frugality is taken out of the equation to allow for higher spending. Fat FIRE still utilizes the 4% withdrawal rule and a high savings rate. In order to determine if Fat FIRE is best for you, ask yourself a few questions and weigh the pros and cons.

Jump Ahead To:

Fat FIRE Is Not Frugal

As a generic rule, Fat FIRE would require about double what the median household income is in the United States. That figure is somewhere in the $50,000 range. Also, keep in mind that that is household income that includes all members living in a household so it takes into account households with more than just one or two people. If you want to Fat FIRE then double the spending to about 100k per year and you will have a pretty spendy upper-middle-class life.

Spending 100k per year is definitely not frugal. Personally, it would be difficult for me to part with that kind of money each year even if I had the means to. The mindset is different with Fat FIRE, as those who seek it may feel that living frugally is a “sacrifice”. Although I have a positive bias towards frugality, I can see their point. Most people wanting to Fat FIRE are going to need incomes at very high levels

How high? Well if their current lifestyle is already spending around 100k a year and they want to save for financial independence then they need to save at least 50% of their income per year. With 100k of spending and 50% savings, you would need to bring in 200k per year. (100k is 50% of 200k). There is a very small percentage of the population that is able to earn this much money per year. If you are one of them then congratulations, Fat FIRE might be just the thing for you.

Fat FIRE doesn’t care about optimizing your lifestyle as regular FIRE does. Those that seek it want things like fancy vacations, fancy cars, fancy houses, and other fancy toys. I use the word “fancy” condescendingly, but really it just means things that are not simple. Fat FIRE gives you the options to spend more on things that regular FIRE just doesn’t.

Fat FIRE Follows Other Rules Of Regular FIRE

It’s not all different, after all for one to be financially independent, they must follow the basic rules in order to get there in a reasonable amount of time. The only thing that really changes is the level of spending and therefore the worth of investments required to generate that level of spending safely. One such basic rule that is still followed is the 4% safe withdrawal rate.

If you don’t know what the 4% withdrawal rate is or need a quick refresher; the 4% safe withdrawal rate is the amount you can withdrawal from your investments each year while still allowing your investments to last nearly indefinitely. The reverse way of calculating how much money in investments you will need for retiring early is to multiply your annual spending by 25. For the example of Fat FIRE spending, 100k per year would require $2,500,000 (100,000 x 25 = 2,500,000) and the 4% way of calculating it would be the same $100,000 ($2,500,000 x .04 = 100,000).

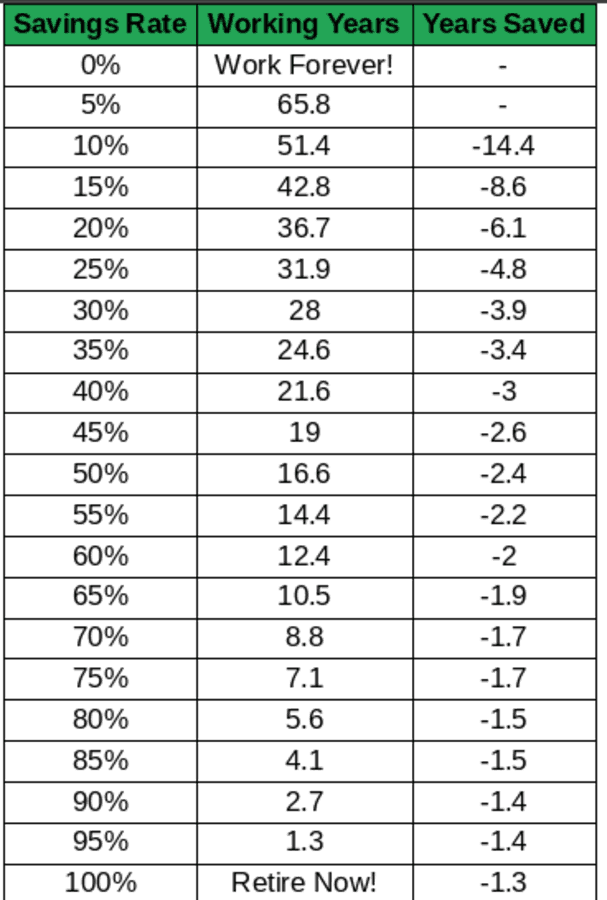

The other requirement that Fat FIRE must follow is a high savings rate because the percentage of your income that you are allowed to save and invest will determine how long it will take you to reach financial independence. As explained in this classic MMM article about “The Shockingly Simple Math Behind Early Retirement” your savings rate determines how long you need to keep working before you can retire early. The law of diminishing returns does set in with savings rates but it is amazing that a 5% increase in your savings could shave several years off of your working career. I have recreated the early retirement chart here:

With a higher level of spending, it is more difficult to achieve higher levels of savings rates unless your income is incredibly high, and we already know that to get to just a 50% savings rate with Fat FIRE your income would need to be at least 200k. Easily this would put you high into the top 10% of earners in the country. Yet you would have to work for 16.6 years to achieve financial independence on a 50% savings rate. If you are serious about financial independence then 10 years is a good goal, but it does entail at least a 65% savings rate.

Is Fat FIRE best for you?

You need to ask yourself honestly if Fat FIRE is even possible for you in the first place. If you are making a median income of $50,000 then how long is it going to take you to reach $2,500,000? A pretty long time, and at that point, it won’t be early retirement anymore. If you are fortunate to be in the top 10% of income earners in the country then you have a bit more options. In order to decide if Fat FIRE might be right for you, weigh out the primary pros and cons;

Pros (compared to regular FIRE):

- With Fat FIRE you do not really have to worry about money. Sure you might do some very basic budget monitoring, but analyzing your spending to the dollar is completely unnecessary. You can almost spend to your heart’s desire (within reason of course) and while it could be easy to spend $100k in a year (many people do it) your lifestyle is most likely to be one of little concern regarding your cash flow.

- You actually retire rich. You’re a multimillionaire. More people are millionaires than ever before, but how much of those millionaires have their money tied up completely in an expensive home? How many of those millionaires are barely over the 1 million dollar mark. How old are these millionaires? Most of them aren’t likely to be early retirees, they are more likely to have been working for many years.

Cons (compared to regular FIRE):

- Fat FIRE will take much longer to reach. Without a frugal mindset, it is difficult to achieve high-level savings rates. With a 50% savings rate, it still takes 16.6 years of working to reach financial independence. An average FI goal is about 10 years from the start by comparison. Even so, you need an unrealistically high income to get a 50% savings rate and spend 100k per year. The barrier to the top 10% of earners is “only” 120k if you spend 100k that is 20k to invest, which is closer to a 15% saving rate. That would be a “normal” working career of 42.8 years!

- You need an unusually high income. The top 5% of earners are around 300k. Now we are talking. If you are in this elite group then maybe you stand a chance of making the savings rates work. For the rest of us, it’s better to adopt a basic frugality mindset.

Ask yourself these questions to see if Fat FIRE is right for you:

- Is your income extremely high? (200k+)

- Is your spending high (100k+) and you want to keep it that way?

- Do you like to travel in luxury?

- Do you drive new cars and don’t want to give it up

If you answer yes to all of these questions then Fat FIRE suits you well. Either that or working for the rest of your life suits you well. Okay, putting biases aside, Fat FIRE would be the ultimate form of easy living, but you still should ask yourself what is important to you, is it the spending, or is it the time you get from financial independence. Fat FIRE is for those that want to be rich, and financial independence is different, it is about much more than money. It’s about freedom, I hope you have gained some insight into Fat FIRE and what it’s all about

Conclusion

Fat FIRE is for high spenders and super-high incomes. It would allow you to live a more luxurious lifestyle because it takes frugality out of the equation. It really is only possible for a small percentage of the population to achieve Fat FIRE. Most people could get to the level of spending that Fat FIRE entails, but it would take a much longer time frame than typical FI goals. Fat FIRE follows all the other same rules as regular FI besides the number just being bigger. Ask yourself what’s important to you, if Fat FIRE is something that fits you best, then I say go for it!